Thought pieces

UK SRS – what next? How companies can prepare

“We’re already collecting ISSB examples and looking at best practices from all over the world to analyse patterns and structures that our clients can leverage.”

Read time: 5-6 mins

Although the FCA’s response to their consultation on the UK Sustainability Reporting Standards (“UK SRS”) is still being finalised, the direction of travel and level of expectation is becoming clearer.

In our last blog “UK SRS – what now?”, we discussed the content of the proposals.

The real question for many companies now is how they can start preparing. But first, let’s recap how we got here.

Why?

The FCA is currently reviewing consultation feedback on how the UK SRS will be implemented, the final step in translating the ISSB’s sustainability reporting standards into a UK context.

The intention is to bring the UK’s fragmented mix of mandatory climate-related financial disclosures, tailored company-specific strategies and voluntary frameworks towards a new global baseline.

With the exception of Europe, which has developed its own framework under CSRD, most major markets are converging around ISSB standards – with countries such as Australia, Japan, Turkey, Brazil and Mexico having already adopted them.

In that context, the UK is in good company, joining countries such as South Korea, Morocco and Bangladesh in signalling adoption.

Although we’ve heard mixed opinions, the government’s choice is far from a standalone initiative, but more so part of a broader movement towards the truly comparable, consistent standards long overdue in sustainability reporting.

When?

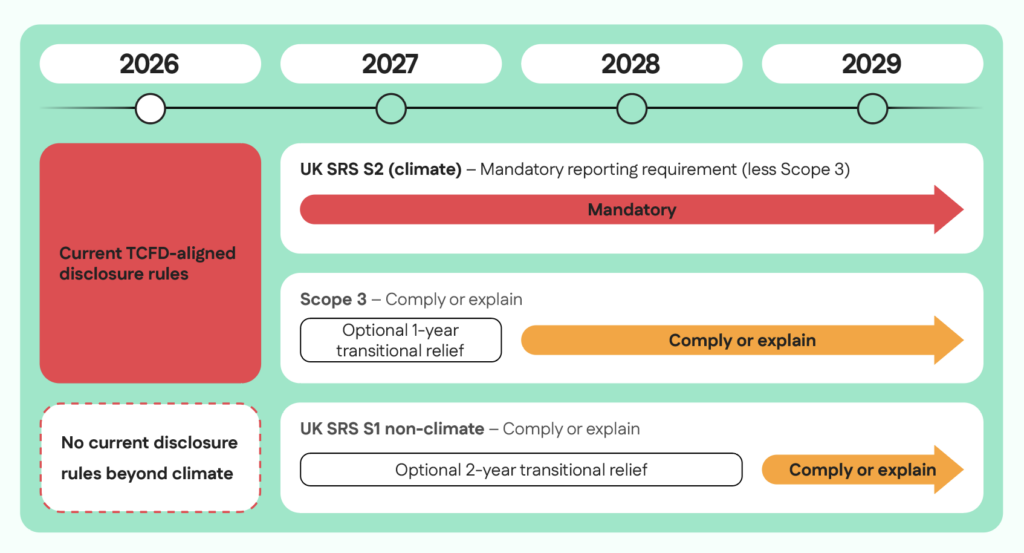

Here’s a recap of the FCA’s proposals.

From accounting periods commencing on or after:

- 1 January 2027: UK SRS S2 (climate) disclosures are mandatory, replacing the TCFD. Scope 3 is comply or explain (or one year of transitional relief). UK SRS S1 (general sustainability) disclosures are comply or explain (or in the first of two years of transitional relief).

- 1 January 2028: Scope 3 is now comply or explain, and UK SRS S1 is on its second and final year of transitional relief.

- 1 January 2029: UK SRS S1 is now comply or explain.

UK SRS reporting timeline adapted from page 11 of the FCA’s consultation document.

A note on materiality

The standards require a single or financial materiality lens, that is, any sustainability-related risks or opportunities that could reasonably be expected to affect the entity’s cash flows, its access to finance or cost of capital in the short, medium or long term. This contrasts with the EU’s double materiality, which also includes external impacts.

This “outside-in” lens could be a useful lever in garnering interest with internal, financially minded stakeholders – and should help create a sharp focus on issues that matter to the company’s success and its longevity.

A key challenge companies will face is collecting relevant, verifiable and comparable data and making it audit-ready – a skillset that finance teams may need to share with other departments when gathering non-financial data.

Ultimately, ascertaining financially material areas for S1 is the most important first step in focusing disclosures on what matters most to your company, and, therefore, investors.

Although the UK SRS make references to the Sustainability Accounting Standards Board (“SASB”) standards optional, they are still a valuable industry-specific set of financially material measures. They offer a standardised starting point for companies seeking an “oven-ready” template of metrics that are comparable, robust and decision-useful and are worth reviewing if your company is wondering where to start.

Where?

The proposals suggest that the UK SRS disclosures should stay within the mainline annual report, but they can be included by cross-reference. The FCA doesn’t prescribe an exact location but does say that companies need to be clear and transparent with where they are disclosing and why. They also state that all information must be published at the same time, formally identified as the official disclosures and be subjected to the same level of scrutiny, governance and controls.

So, a suitable cross-reference might look like “Our Scope 3 emissions are disclosed in the Climate Databook at example.com/climate2027.pdf – this document is incorporated by reference into this annual report.” It wouldn’t look like “See our microsite for our latest Scope 3 climate data” as this wouldn’t legally form part of the annual report; it wouldn’t be signed off and fixed at the publishing date of the annual report, and it’s not subject to the same level of board oversight.

This may mean that we get used to seeing ISSB compliance index tables in the report, potentially with separate databooks for any lengthy disclosures. Alternatively, trends may move towards integrated reporting, addressing each pillar (strategy, risk, governance, and metrics and targets) alongside more traditionally strategic, governance and financial disclosures in the annual report. Or perhaps UK reporting could be influenced by European CSRD trends and include a lengthy sustainability statement within the annual report.

This adaptable approach empowers companies to report in a way that works for them and to incorporate additional frameworks and standards. However, this flexibility can give rise to a state of trepidation as to whether companies are reporting in the right way, place or structure. We know that some forward-facing clients have attempted to add in ISSB-aligned disclosures previously, only to have auditors ask for them to be removed as they’re not yet ready to form an opinion.

That’s why lyonsbennett’s benchmarking service is so valuable; we’re already collecting ISSB-aligned examples and looking at best practices from all over the world to analyse patterns and structures that our clients can leverage.

Although clear expectations are always welcome, a one-size-fits-all approach rarely works in practice (read up on the CSRD’s Omnibus for what happens when plans are too ambitious, wide-reaching and challenging without extensive prior consultation before rollout).

Lyonsbennett will be monitoring the consultation responses, rollout and developing practice closely, and we’ll be here to work things out with you and our trusted partners to ensure your reporting remains compliant while telling your company’s story. You can contact us to chat through at any time by reaching out to your project manager or contact us on hello@lyonsbennett.com.

How?

What other steps can companies take to prepare?

- Read the UK government’s finalised standards and the FCA’s consultation to review the proposals. Note, the FCA’s consultation closed on 20 March 2026.

- Conduct a financial materiality assessment to ascertain the risk and opportunity areas for your business in the short, medium and long term.

- Conduct internal readiness assessments, with or without external sustainability support.

- Decide which data you will need to collect based on financially material areas – will you use SASB?

- Build and test data collection systems that align with the requirements of S1 and S2.

- Build a phased roadmap towards future compliance.

- Work together – sustainability reporting today requires whole-business collaboration.

- Ask questions and educate!

Best practice will evolve in this emerging area, and we’re all in this together. If you’d like an invitation to our next lyonsbennett virtual roundtable with a global sustainability activator, where we’ll run through the implications of the proposals, examples of current reporting and answer your questions, please get in touch.